The Energy Trading Gamble!

September 02, 2015

on

on

Did you know that energy traders are playing a vital part in keeping Europe’s energy prices competitive and supplying countries with their energy needs? They are integral to the business of buying and selling of energy commodities such as power, gas and oil and their delivery from where they are produced to where they are consumed. How this is accomplished, is completed in a number of different ways (examined in detail below). However, as in any established market, the procedure conforms to the essential principle of negotiating and settling differences in the price of such commodities between markets. Energy traders act as intermediaries between energy suppliers and potential buyers. “They are very useful at finding the energy supplies in the quantities that customers want,” says Nigel Harris of Energy Consultant, Kingston Energy. Energy traders are also used for hedging energy prices and quantities against seasonal trends and unfavourable developments in the market, such as anticipated disruption of Russian gas supplies to Europe or a hotter than expected summer. This feature will focus on power and gas trading in Europe.

Development of European energy trading

According to Harris, energy markets exploit all forms of negotiation, starting with bilateral trading where there is no broker involvement and traders contact each other directly, creating deals on a one-to-one basis. At another level, there is “voice and email broking” with traders contacting the energy trader directly rather than each other and trading becomes even more multi-lateral with offers being shown to multiple potential counterparties. As markets become more active and liquid, the need for negotiation lessens. Through the traders, buyers can quickly find a willing seller and vice-versa. Competition between traders ensures that the prices offered are reasonable and the spread between the bid and offer price becomes quite narrow. It can also be almost instantaneous with screen trading in which sellers advertise their offer price and buyers show their bid price and deals are concluded by the click of a mouse.

The European Federation of Energy Traders (EFET), established in 1999 in response to the liberalisation of the EU’s electricity and gas markets, has 126 member companies from 27 European countries and they trade standard products in wholesale electricity and gas forward and spot markets. Likewise, The London Energy Brokers Association members trade in European gas and power in both the over-the-counter markets and European exchanges. Fundamentally, traders intermediate and facilitate bilateral contracts between banks, trading houses, commercial enterprises, utilities and energy companies. Energy traders work for specialist independent firms, also for trading subsidiaries of many major financial institutions, energy producers and energy retail distribution companies.

Trading occurs through various designated exchanges as well as “off the exchanges” through over-the-counter electronic trading and in direct trading between two contract partners over the phone. Europe has about a dozen exchanges, the most important of which are the European Energy Exchange (EEX) in Leipzig, Nord Pool in Oslo and ICE for futures and over-the-counter trading in London.

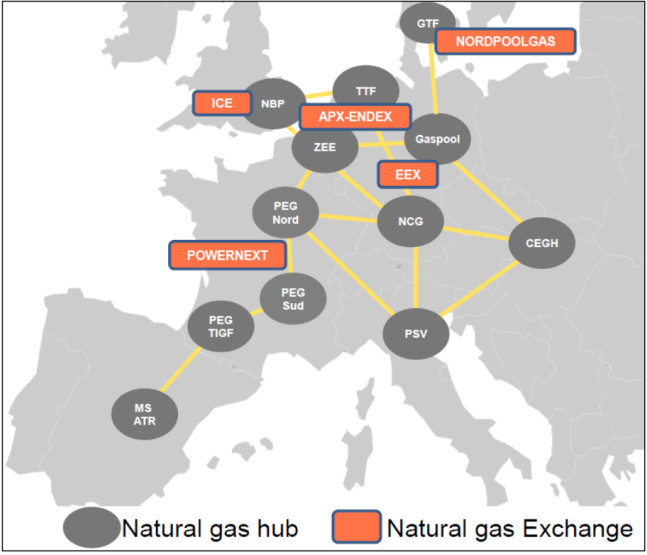

Standard products are offered on regional exchanges and trading takes place anonymously, i.e. seller and buyer do not know each other. “Clearing” guarantees the financial integrity of a contract on the exchange. However, the majority of dealings take place outside designated exchanges in so-called over- the-counter trades (OTC) in which the participants buy or sell individual products through electronic screen trading says RWE’s analyst, Anna Katharina Obertacke. As for gas, according to Obertacke, “Trading gas in Europe is special. The largest volume of trade takes place via virtual trading points (hubs). See Figure 1. No physical gas flows there but this is where contract partners do their deals.” Important hubs are the National Balancing Point in the UK and the Title Transfer Facility in the Netherlands.

Figure 1. European gas hubs and gas exchanges

Source: OxfordEnergy.org

A case in point is that of the Nord Pool Spot exchange, which operates throughout Scandinavia, the Baltic States, plus Germany and the UK, servicing some 370-power companies. More than 80% of the 420 Terra Watt hours (TWh) total consumption of electrical energy in the Nordic market is traded through Nord Pool Spot. It has the distinction of being the world's first multinational exchange for trading electric power, derived from a variety of power generation technologies. See Figure 2. Nord Pool Spot offers both day-ahead and intra-day markets and is owned by the participating national grid companies.

Figure 2. Nord Pool spot exchange

Source: NordPoolSpot.com

In Europe’s energy markets, electricity and gas are treated as commodities, although gas can be stored whilst electricity cannot. This means that a quantity of electricity can be sold today for delivery at an agreed date and time and then billed. The exchanges offer three main types of trade. These are:

(a) Spot markets, where buying takes place on one day and selling on the following day, or the subsequent week or in the ensuing month.

(b) Forward market - these assign physical delivery of electricity or gas to a future date.

(c) Future markets, which indicate at the close of each day what the market price for electricity will be on a specified date in the future - for example in the following year.

Any difference between the predicted and the ultimate buying price is settled in cash on the delivery date and will show each party to the transaction if their “bet” has paid off. Traders in this, as in all commodity markets, are always on the lookout for opportunities to make financial gain from the “difference” – which can be conditioned by geography, weather and unforeseen accidents of politics and decisions of the European Parliament.

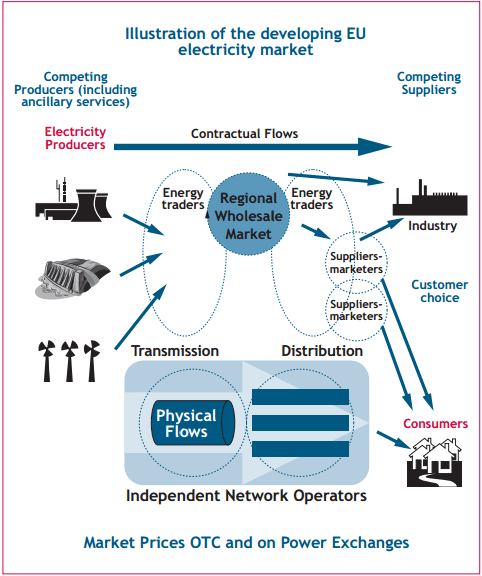

In addition to unpredictable hazards, traders must take account of the complex problems posed by the physical transport of energy. To move energy across markets traders and marketers must purchase transmission and gas transport space from transmission providers and pipeline owners. Essentially, energy products are physically traded: an actual amount of electricity or gas is bought, delivered at an agreed date and time and billed. An outline of the participants in Europe’s electricity and gas markets can be seen in Figure 3.

Figure 3. How the EU electricity market works –note the gas market is similar

Source: Efet.org

In Europe’s leading energy exchange, EEX some 586 TWh of electricity was traded in 2014. In the same year, The London Energy Brokers Association records show members trade in Europe’s OTC market and European exchanges at 17,196,931.057 Million Watt hours of gas and 7,150,066,990 (MWh) of power. These volumes revealed a marked decline in levels of trade from 2011. As Harris remarks, “in the early years energy-trading opportunities were good. However, recession and the rise of renewables reduced demand and price differentials thereby reducing trading”. Harris notes that trade has “started to pick up in Europe, due declines in gas prices and increasing uncertainty caused by the ongoing Russian Ukraine dispute”.

A recent report from the Italian Bruno Leoni Institute (“Index of Liberalisations”) revealed significant barriers to competition including different regulations and levels of subsidies. For example, whilst Britain is the most open to free market trading, Spain, Italy and Northern Europe are restrictive says Peter Styles, Chairman of the EFET’s Electricity Committee. The existence of different levels of subsidy and derogations to member states impairs competition: a case in point is the differing national rates of subsidy for renewables which has directed investment flows to where the subsidies are highest, rather than to where it is windiest or sunniest.

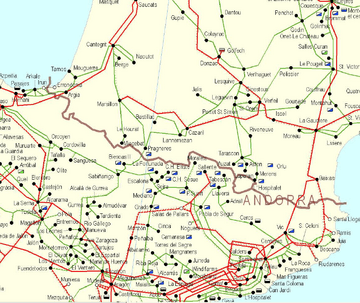

Being able to physically store and trade energy from one market is not without its problems due to a lack of a common set of technical rules and trading arrangements to ensure that power flows across the continent’s wires and pipes from the cheapest sources to markets with the highest prices. Currently also, insufficient number of gas and power interconnectors limit trading opportunities. For example insufficient interconnector capacity between the Iberian Peninsula and France severely restricts Spain’s energy exports to the rest of Europe. See Figure 4.

Figure 4. The different interconnection lines between France and Spain

Source: Cigre.org

The prospect of new tough financial and market regulatory measures relating to capital reserves, cost of licences and a larger risk management workforce are seen as potential obstacles to successful energy trading by Styles. In the meantime Stephen Woodhouse, Energy Consultant at Poyry suggests introducing flexible trading instruments such as options and ensuring that Transmission System Operators offer interconnector capacity across a range of timeframes, including forward and also intra-day rather than just day-ahead times, would prove advantageous and help energy traders to continue to play a vital role in ensuring that power and gas gets to the customer at the right place, the right time and the right price.

Image: EEX trading room. Courtesy EEX.

Development of European energy trading

According to Harris, energy markets exploit all forms of negotiation, starting with bilateral trading where there is no broker involvement and traders contact each other directly, creating deals on a one-to-one basis. At another level, there is “voice and email broking” with traders contacting the energy trader directly rather than each other and trading becomes even more multi-lateral with offers being shown to multiple potential counterparties. As markets become more active and liquid, the need for negotiation lessens. Through the traders, buyers can quickly find a willing seller and vice-versa. Competition between traders ensures that the prices offered are reasonable and the spread between the bid and offer price becomes quite narrow. It can also be almost instantaneous with screen trading in which sellers advertise their offer price and buyers show their bid price and deals are concluded by the click of a mouse.

Energy traders

The European Federation of Energy Traders (EFET), established in 1999 in response to the liberalisation of the EU’s electricity and gas markets, has 126 member companies from 27 European countries and they trade standard products in wholesale electricity and gas forward and spot markets. Likewise, The London Energy Brokers Association members trade in European gas and power in both the over-the-counter markets and European exchanges. Fundamentally, traders intermediate and facilitate bilateral contracts between banks, trading houses, commercial enterprises, utilities and energy companies. Energy traders work for specialist independent firms, also for trading subsidiaries of many major financial institutions, energy producers and energy retail distribution companies.

Trading occurs through various designated exchanges as well as “off the exchanges” through over-the-counter electronic trading and in direct trading between two contract partners over the phone. Europe has about a dozen exchanges, the most important of which are the European Energy Exchange (EEX) in Leipzig, Nord Pool in Oslo and ICE for futures and over-the-counter trading in London.

Standard products are offered on regional exchanges and trading takes place anonymously, i.e. seller and buyer do not know each other. “Clearing” guarantees the financial integrity of a contract on the exchange. However, the majority of dealings take place outside designated exchanges in so-called over- the-counter trades (OTC) in which the participants buy or sell individual products through electronic screen trading says RWE’s analyst, Anna Katharina Obertacke. As for gas, according to Obertacke, “Trading gas in Europe is special. The largest volume of trade takes place via virtual trading points (hubs). See Figure 1. No physical gas flows there but this is where contract partners do their deals.” Important hubs are the National Balancing Point in the UK and the Title Transfer Facility in the Netherlands.

Figure 1. European gas hubs and gas exchanges

Source: OxfordEnergy.org

A case in point is that of the Nord Pool Spot exchange, which operates throughout Scandinavia, the Baltic States, plus Germany and the UK, servicing some 370-power companies. More than 80% of the 420 Terra Watt hours (TWh) total consumption of electrical energy in the Nordic market is traded through Nord Pool Spot. It has the distinction of being the world's first multinational exchange for trading electric power, derived from a variety of power generation technologies. See Figure 2. Nord Pool Spot offers both day-ahead and intra-day markets and is owned by the participating national grid companies.

Figure 2. Nord Pool spot exchange

Source: NordPoolSpot.com

Types of trades

In Europe’s energy markets, electricity and gas are treated as commodities, although gas can be stored whilst electricity cannot. This means that a quantity of electricity can be sold today for delivery at an agreed date and time and then billed. The exchanges offer three main types of trade. These are:

(a) Spot markets, where buying takes place on one day and selling on the following day, or the subsequent week or in the ensuing month.

(b) Forward market - these assign physical delivery of electricity or gas to a future date.

(c) Future markets, which indicate at the close of each day what the market price for electricity will be on a specified date in the future - for example in the following year.

Any difference between the predicted and the ultimate buying price is settled in cash on the delivery date and will show each party to the transaction if their “bet” has paid off. Traders in this, as in all commodity markets, are always on the lookout for opportunities to make financial gain from the “difference” – which can be conditioned by geography, weather and unforeseen accidents of politics and decisions of the European Parliament.

In addition to unpredictable hazards, traders must take account of the complex problems posed by the physical transport of energy. To move energy across markets traders and marketers must purchase transmission and gas transport space from transmission providers and pipeline owners. Essentially, energy products are physically traded: an actual amount of electricity or gas is bought, delivered at an agreed date and time and billed. An outline of the participants in Europe’s electricity and gas markets can be seen in Figure 3.

Figure 3. How the EU electricity market works –note the gas market is similar

Source: Efet.org

In Europe’s leading energy exchange, EEX some 586 TWh of electricity was traded in 2014. In the same year, The London Energy Brokers Association records show members trade in Europe’s OTC market and European exchanges at 17,196,931.057 Million Watt hours of gas and 7,150,066,990 (MWh) of power. These volumes revealed a marked decline in levels of trade from 2011. As Harris remarks, “in the early years energy-trading opportunities were good. However, recession and the rise of renewables reduced demand and price differentials thereby reducing trading”. Harris notes that trade has “started to pick up in Europe, due declines in gas prices and increasing uncertainty caused by the ongoing Russian Ukraine dispute”.

Lack of a free market hurts energy trading

A recent report from the Italian Bruno Leoni Institute (“Index of Liberalisations”) revealed significant barriers to competition including different regulations and levels of subsidies. For example, whilst Britain is the most open to free market trading, Spain, Italy and Northern Europe are restrictive says Peter Styles, Chairman of the EFET’s Electricity Committee. The existence of different levels of subsidy and derogations to member states impairs competition: a case in point is the differing national rates of subsidy for renewables which has directed investment flows to where the subsidies are highest, rather than to where it is windiest or sunniest.

Being able to physically store and trade energy from one market is not without its problems due to a lack of a common set of technical rules and trading arrangements to ensure that power flows across the continent’s wires and pipes from the cheapest sources to markets with the highest prices. Currently also, insufficient number of gas and power interconnectors limit trading opportunities. For example insufficient interconnector capacity between the Iberian Peninsula and France severely restricts Spain’s energy exports to the rest of Europe. See Figure 4.

Figure 4. The different interconnection lines between France and Spain

Source: Cigre.org

Ongoing improvements and prospects

The prospect of new tough financial and market regulatory measures relating to capital reserves, cost of licences and a larger risk management workforce are seen as potential obstacles to successful energy trading by Styles. In the meantime Stephen Woodhouse, Energy Consultant at Poyry suggests introducing flexible trading instruments such as options and ensuring that Transmission System Operators offer interconnector capacity across a range of timeframes, including forward and also intra-day rather than just day-ahead times, would prove advantageous and help energy traders to continue to play a vital role in ensuring that power and gas gets to the customer at the right place, the right time and the right price.

Image: EEX trading room. Courtesy EEX.

Read full article

Hide full article

Discussion (0 comments)